2.1 This section of the Local Plan provides an account of the issues facing the Mendip area as distilled from the background evidence that has been used to inform this plan. By exploring the issues that arise across the area, this offers context and establishes the basis for the subsequent policy statements and proposals contained later in the plan.

2.2 Mendip is a rural district, covering an area of 738 square kilometres. The district contains five principal towns: Frome, Glastonbury, Shepton Mallet, Street and Wells. They each function as ‘market towns’ and meet a high proportion of the everyday needs of their residents and those of their rural catchments. There are in excess of 100 smaller rural settlements, varying in size from the largest villages like Coleford and Chilcompton (population circa 2,000) through to the smallest of hamlets which may consist of a dozen or so houses. In 2006, the base date for this strategy, the district had an estimated population of 108,300 with around two thirds living in the five main centres. Frome is the largest town while Glastonbury is the smallest.

FIGURE 1 : Mendip District in Context

2.3 Whilst containing five towns of varying characteristics, the district is influenced by centres that lie outside its boundaries to greater or lesser degree. To the south and west, Yeovil and Taunton draw trade and workers from the area to some degree, however Bristol and Bath to the north have a much greater degree of influence. They attract commuters to comparatively better paid jobs, shoppers for a wider choice of higher order goods and place pressures on local housing markets. The market towns of Midsomer Norton and Radstock, in Bath and North East Somerset, immediately adjoin the northern boundary of the district and meet some of the needs of residents of nearby Mendip villages.

2.4 Frome and the rural communities to the east of the district have strong links with the Wiltshire towns of Trowbridge, Westbury and Warminster, facilitated by road including the A36/A350 corridor and rail links via Westbury.

2.5 Commuting and a workforce to meet the needs of business were highlighted as significant issues during consultation. In light of the fact that the census remains the only true means of assessing flows between work and residence the Council has had to rely on 2001 census data, supplemented by commentary in the 2009 West of England Strategic Housing Market Assessment as well as survey data gathered from the latest 2012 Mendip Housing Needs Assessment. The figures below, whilst dated, give an idea of the scale of outflows to each place which are not considered to have changed significantly since the data was recorded.

2.6 The level of net out commuting is a particular issue for Frome with around 2,500 commuters travelling to Bath and the west Wiltshire towns whilst reverse flows are substantially lower as indicated in Table 1a below. As a result the town has the lowest ratio of jobs to economically active population of any of the main centres.

| Mendip | Frome | G’bury/Street | Shepton | Wells | |

| West Wiltshire | 1350 | 1245 | 42 | 29 | 35 |

| B&NES | 2104 | 1660 | 107 | 258 | 80 |

| Bristol | 1185 | 325 | 131 | 279 | 450 |

| N Somerset | 282 | 59 | 48 | 68 | 106 |

| S Gloucestershire | 399 | 189 | 68 | 57 | 87 |

| Somerset & Other South West |

-62 | 527 | -350 | -126 | -112 |

| Other Areas | -95 | 375 | -492 | 144 | -122 |

| TOTAL | 5163 | 4380 | -448 | 709 | 524 |

TABLE 1a : Net Commuting Flows to / from adjacent areas (2001 Census/2009 West of England SHMAA)

2.7 In the other towns, actual and net commuting flows are not as significant particularly when the local Mendip labour force is factored in as shown in Table 1b. The exceptions to this are Glastonbury/Street and Wells. At Street, specifically, there was a substantial inflow (signified by the negative figures in the table above) of workers from other areas, notably other parts of Somerset. At Wells, the net outflow of 524 employees to areas outside Mendip masks a far more dynamic flow of labour which sees around 2500 workers commute out to Bristol/Bath and other destinations in Somerset with around 1900 travelling in – half from Bristol/Bath and half from other locations in Somerset. Local labour flows within the district showed that Wells drew in almost 1000 employees from other towns.

| Work in…. | |||||

| Live in… | Frome | Glastonbury / Street | Shepton | Wells | |

| Frome | 10122 | 207 | 758 | 203 | |

| G’bury / Street | 156 | 8100 | 559 | 862 | |

| Shepton | 451 | 318 | 4582 | 833 | |

| Wells | 171 | 614 | 763 | 5342 | |

| NET FLOW | 391 (out) | 437 (out) | 479 (in) | 963 (in) | |

TABLE 1b : Commuting Flows within Mendip (2001 Census/2009 West of England SHMAA)

2.8 In terms of travel for goods and services, the 2010 Mendip Town Centres study indicates that Mendip performs relatively well with 88% of its residents convenience shopping needs (food, everyday purchases) met within the district. 55% of comparison goods (e.g. clothes, shoes, electrical goods, furniture, DIY, garden, etc.) are also bought within Mendip with 14% of the remainder obtained from online sources. In common with work patterns, Bristol, Bath, Yeovil and Taunton attract trade away from the district although this is accepted to be as a result of the wider range and choice available in these larger centres.

2.9 In terms of future needs, the 2010 study indicated that there would be plenty of spending capacity to support town centre regeneration in all of the towns within the non-food sector. However, a significant change in the outlook for retail and the extended role that online retailing will play in the future means that the emphasis must be upon schemes which complement the existing offer and extend consumer choice – in essence making town centres attractive, convenient and well designed shopping and leisure destinations.

2.10 In terms of food store provision, capacity to 2021 – a reliable future horizon – is limited on account of existing operators and consents recently granted in Glastonbury and Wells. Any future stores will be predicated on competition rather than absolute need for them. Scope for better food stores in town centre locations which attract shoppers to purchase food and goods from other shops exist, however a fine balance is needed to ensure the wider vitality and functioning of those centres is maintained, and regeneration of sites in Frome will need to be especially cautious in this respect.

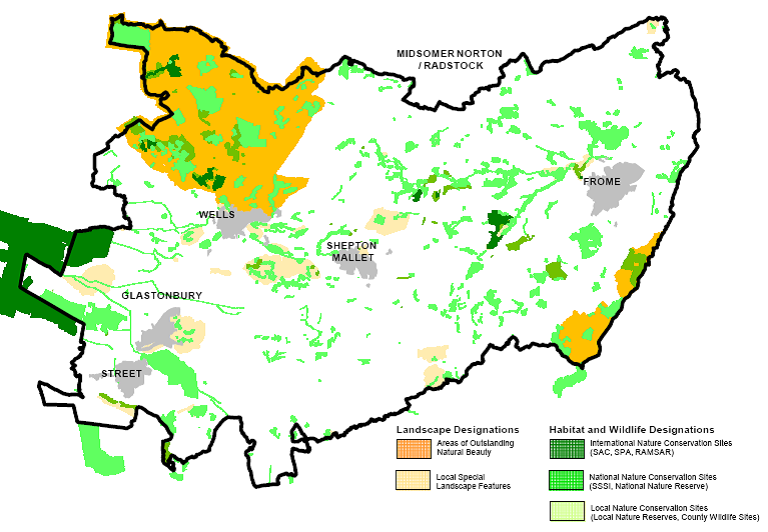

2.11 Mendip’s natural and man-made environments are highly diverse and this is a distinctive feature of the district. The complex geology, topography, hydrology and geography of the area have resulted in habitats and landscapes of distinctive character and high visual quality. There is a wealth of internationally, nationally and locally designated sites of wildlife value as well as important designated geological sites.

FIGURE 2: The Extent of Designated Landscapes and Wildlife Sites across Mendip District

2.12 The Mendip Hills give the district its name and part of the hills form the Mendip Hills AONB. This high landscape quality forms part of the setting for the City of Wells and contributes to the strong sense of place. Three of the district’s EU Special Areas of Conservation (SAC) are associated with the Mendip Hills and their extensive cave systems which provide important habitats for bat species. Furthermore, the area around Priddy in the north west of the district has one of the highest concentrations of Scheduled Ancient Monuments. The Mendip Hills are also one of the UK’s principal sources of high quality hard Carboniferous Limestone rock and the district contains seven active quarries. Most of these lie between Shepton Mallet and Frome, producing around 12 million tonnes per year, and indirectly employ 1,500 people across varied sectors.

2.13 Since the late 1990s, a new process called Hydraulic Fracturing, sometimes shortened to “Fracking” has emerged which is capable of allowing the recovery of pockets of hydrocarbons from rock strata. The process, very simply, involves injecting fluid at high pressure into rock formations to propagate cracks and fractures which in turn releases gas (of varying forms including natural gas and coal seam gas) which can then be extracted. In recent years, assessments in the UK have revealed that there may be potential in the Mendip Hills for the extraction of gas using this method. The government is granting exploration licences, but commercial exploitation would be planned and managed through Somerset County Council’s Minerals Plan. The District Council expects that a precautionary principle is applied by bodies considering the use of this technique given the importance of the area’s geology on water supply, landscapes and biodiversity. Until the impacts, localised and area wide, including knock on effects on tourism, are understood the Council will not support this form of development.

2.14 In contrast to the Mendip Hills are the Somerset Levels and Moors - a low lying plain modified by man over centuries to create grazing land drained by interlocking ditches, known as rhynes. A significant proportion of the Levels and Moors is designated as an EU Special Protection Area (SPA), primarily on account of its birdlife interest. The area is also internationally recognised for discoveries of prehistoric remains that lie preserved in the peat.

2.15 The Cranborne Chase and West Wiltshire Downs AONB fringes the eastern side of the district offering panoramic views across the undulating countryside which formerly made up the ancient Selwood Forest.

2.16 The geology, topography and geography of the district have had a direct bearing on the pattern of settlement and communication. The resulting diversity has contributed to the tremendous variation of settlement layout and building styles. These generate a varied sense of place and true local distinctiveness ranging from the Arts and Crafts style worker’s housing built from Blue Lias in Street, to the distinctive honey coloured historic buildings of Frome. As a result, and recognising the extensive heritage, there are 27 conservation areas and nearly 3,000 listed buildings in Mendip. These features are important culturally and economically.

2.17 The Levels and Moors form a substantial area at high risk of fluvial flooding and this affects Glastonbury and its surrounding villages. Flash flooding, caused by surface run-off is also a problem in some areas, especially Shepton Mallet. In the future, acknowledging climate change effects, flood risk areas will be more prone to incident and pressure on drainage systems in areas where flood risk is less prevalent may still result in localised inundation.

2.18 In terms of the 2006 population, observable existing variations from national averages were that there was under-representation of 16-30 year olds primarily based on the movement of school leavers from the area for higher education, employment or career progression. Conversely, pre-retirement age groups (50-60) were over-represented as these groups migrate into the area from urban districts.

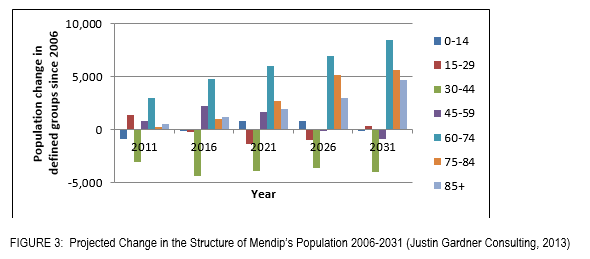

2.19 Figure 3 reveals the trends likely to occur over the next 20 years. It indicates that the decline in younger age groups will continue. More dramatic however, is the growth in age groups aged over 60 which by 2029 will have increased its share of the district population from 27% in 2011 to 36% with the number of people aged 90 or more trebling to over 3,000.

2.20 A clear implication of the latter trend is that the number of households will grow and, furthermore, the average household size is set to fall as retired couples and widow(ers) households make up a larger share of all households as illustrated in the table below.

Frome |

G’bury |

Street |

Shepton Mallet |

Wells |

Rural Area |

Total |

|

2011 Population 2011 Households 2011 Economically Active |

26,223 11,205 14,088 |

8,943 4,040 4,616 |

11,820 4,771 5,730 |

10,374 4,378 5,926 |

10,556 4,917 4,981 |

41,489 16,900 21,551 |

109,406 46,212 56,893 |

2029 Projected Population 2029 Projected Households 2029 Economically Active |

30,365 13,582 15,768 |

9,819 4,644 4,794 |

12,938 5,716 6,283 |

12,276 5,496 6,633 |

10,542 5,095 4,873 |

44,474 18,988 21,791 |

120,414 53,520 60,141 |

TABLE 2: SNPP updated – based on population projection (Mendip Housing Requirements Study 2013)

2.21 As implied from the 2011 average household sizes, to some degree this trend is already advanced in Wells which has a markedly older age structure than that of the rest of the district, save for some rural communities. In response to these trend based projections, there is a clear argument that pure application of household growth will only perpetuate trends, in turn justifying levels of new housing provision that improves the inherent balance of economically active people and jobs.

2.22 Indicators of health are generally good in comparison to the averages for England. Mendip residents have life expectancies in line with the national average of 78.1 years (England - 77.3) for men and 82.4 (England – 81.5) years for women. Although the district is a prosperous area there are pockets of deprivation as recorded in the Indices of Deprivation. The main areas are Street North, Shepton East, Frome Welshmill, Glastonbury St John’s and Glastonbury St Benedict’s.

2.23 The number of dwellings in the district in 2006 was 46,933 and at that time around 1,250 homes, 2.5% of the total, were vacant. In 2012, that figure had risen to 1,441, although under a more meaningful measure – those vacant for longer than six months – the figure stands at 445.

2.24 Owner occupation represents the largest share of housing stock, standing at 73% in 2011. 13% are in social rented tenure, with the remaining 14% privately rented. Compared with English averages social rented and private rented properties are marginally underrepresented although the proportions are consistent with South West and Somerset averages. Some commentators have observed that a larger private rented sector has benefits for workforce mobility.

2.25 Affordability of housing is the major issue in Mendip as it is across much of southern England. Between 2001 and 2006 the district experienced some of the largest house price rises of any of the local authorities in the West of England area. The average price of a semi-detached house rose by 63%. By the end of this period the proportion of young households able to buy or rent in the market fell to 42%. Whilst affordability of housing has marginally improved as a result of house price falls observed during the 2008-2012 period, all expectations point towards this being a blip as the national housing market continues to be dogged by inconsistent delivery and unrealistic land value expectations. The impact will be most acute on young people and the population change trends shown in figure 3 above will be partly driven by housing affordability.

2.26 The table below summarises the scale of housing need in Mendip for the period to 2016 based on information set out in the latest 2011 Mendip Housing Needs Assessment.

| Net annual affordable housing need | Frome | Glastonbury/ Street | Shepton Mallet | Wells | Rural | Mendip District |

| 145 | 186 | 65 | 67 | 281 | 743 |

TABLE 3: Projected net annual affordable housing need in Mendip’s sub housing market areas 2011-16 (Fig. 7.19 MDC/JGC Housing Needs Assessment, 2011)

2.27 The district total of 743 new affordable homes per year is an unrealistic target for the Council to seek to deliver. Public subsidy for affordable homes is, in the current period of austerity, very scarce. Furthermore, the development industry highlights, quite fairly - up to a point – that development viability cannot support ever escalating levels of affordable housing obligations on the back of market housing. This is recognised nationally and over recent years government has sought to grapple with the issues, making announcements about “affordable rented” tenures, adjusting the benefits regime by bringing in Universal Credit and tackling worklessness. The extent to which these measures will address ever rising demands for affordable homes will become apparent during the lifetime of this Local Plan.

2.28 In considering what the District Council can do to address this matter, the clear starting point is that the delivery of affordable homes must be maximised as far as this is possible to achieve. Development Viability work undertaken to inform this plan provides one means to ensure this can be achieved and, as a headline figure, most development sites should be able to support a 30% requirement (40% at Wells and some rural villages) for affordable homes although in each case, specific circumstances will need to be explored where developers argue this level cannot be achieved.

2.29 In respect of housing delivery, Mendip District was successful over the preceding plan period in making provision for the development industry to build all of the planned housing. The previous Mendip District Local Plan, guided by the Somerset County Structure Plan (1991-2011) made provision for “about 8,950” for that 20 year period. The table below summarises supply towards the targets set out in that plan.

| Somerset

Structure Plan Target Provision (1991-2011) |

Homes Completed (1991-2011) | % of Target Met | Brownfield Completions (2000-2011) | |

| Frome Glastonbury Shepton Mallet Street Wells |

2,590 1,000 1,120 1,135 1,100 |

2,357 1,061 1,338 1,069 1,001 |

91% 106% 119% 94% 91% |

1,257 450 334 394 406 |

| All Towns Rural Areas | 6,980 1,970 |

6,826 2,553 |

98% 129% |

2,841 796 |

| Total | 8,950 | 9,379 | 104% | 3,637 |

TABLE 4: Housing Targets and Completions in Mendip 1991-2011 (Mendip DC Housing Monitoring

2.30 Overall 104% of the target provision has been built although there is some variation between where it was planned and built. This is largely down to the unpredictable supply of brownfield land arising particularly from the restructuring in the local economy in the towns and, in rural areas, infilling and redevelopment promoted during the housing boom. The later than planned release of a major greenfield area at Shepton Mallet coinciding with some modest speculative brownfield development since 2000 led to a modest overprovision of 180 homes, counteracting the under delivery at Frome and Street. In both of the latter however, delays in major sites (Garsdale/Saxonvale and Houndwood respectively) has been the cause.

2.31 Since 2006, the District has been successful in securing 2,131 of the total 3,201 new homes (67%) on brownfield sites to 2013. Land supply data considered in section 4 of this strategy suggests that brownfield sites will continue to play a part in delivering a substantial number of new homes in the period to 2029. However, the supply of such sites is diminishing and so there will be a need for new development to take place on new greenfield sites.

2.32 As a result of Mendip’s geographic position and the large number of festivals that take place within its boundaries, the district is an area of considerable importance for the travelling community. Based upon the Gypsy and Traveller Accommodation Assessment (updated 2013), there is a need for 90 additional residential pitches to 2020 and 51 from 2021-2029. In addition, at least 80 transit pitches may be required in the plan period.

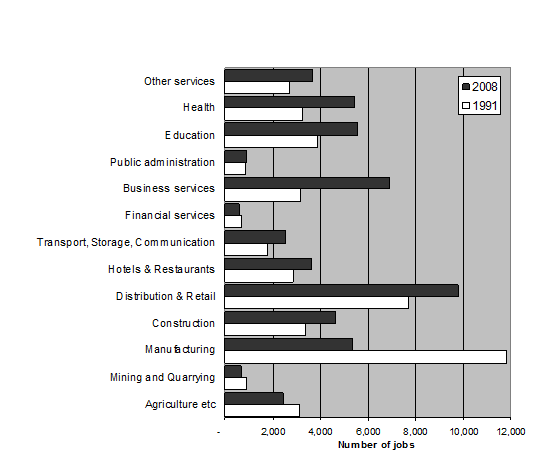

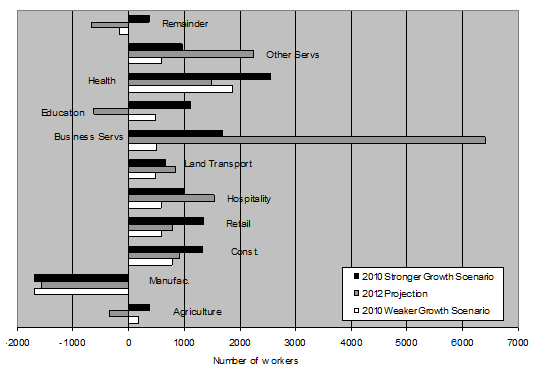

2.33 The economy of Mendip is made up predominantly of micro and small companies and is now largely service based having seen many of its traditional industries decline or move away from the area over the last 20 to 30 years. The diagram below shows the change that has taken place and that the greatest number of jobs are now in distribution, retailing, construction, health, education and business services (such as property management, information technology and professional services). Traditional manufacturing industry has markedly declined which has required some re-skilling of the workforce. Nevertheless, unemployment is low with a rate below the regional and national averages.

FIGURE 4: Change in the structure of Economic Sectors in the Mendip Economy 1991-2008 (MDC/Oxford Economics, 2010)

2.34 Another clear observation is that the local economy is a lower skilled, lower paid one, although it should be noted that this is common to economies across the South West as shown in the table below. Mendip wages are consistent with Somerset averages, about 5% lower than SW averages and 15-20% below the UK average. Whilst regional variations are to be expected, the most significant implication for Mendip is that it nestles up against the West of England where higher wages can be secured. The main effects of this are borne out in relatively higher housing prices and significant commuting patterns.

| % of UK Average | 2000 | 2008 | 2012 | 2020 | 2030 |

|---|---|---|---|---|---|

| Mendip | 85 | 80 | 81 | 80 | 79 |

| South Somerset | 88 | 87 | 83 | 81 | 79 |

| Sedgemoor | 79 | 77 | 77 | 75 | 72 |

| Somerset | 86 | 84 | 82 | 81 | 79 |

| South West | 89 | 90 | 87 | 86 | 85 |

| United Kingdom | 100 | 100 | 100 | 100 | 100 |

TABLE 4a: Comparative Wage Levels (Heart of the West of England

2.35 Despite the prolonged downturn and recession precipitated by the global financial crisis of 2008-09, the longer term prospects for the local economy are good with growth predicted in many sectors. Unsurprisingly, employment in the Business Services sector is expected to grow more than any other with technical and scientific, information, communication and support services being the main drivers. This sector offers significant opportunity within Mendip as employees are less dependent on large scale centralised places of work. Such activities can be remotely based and as a result new business activity has the potential to bring higher value jobs which may reduce some of the commuting trends to places outside the district which have developed since the 1990s. In turn this may enable the local workforce to compete better in the local housing market. Providing improvements in broadband speeds will be crucial in facilitating this.

FIGURE 5:

Projected Job Growth in Mendip to 2030 by Economic

Sector (Oxford Economics/ Mendip DC, 2012)

2.36 Retailing has emerged as a strong component of the local economy which is linked to health and competitiveness of the market towns. By 2030 retailing will be the second largest employment sector. Over the last decade there has been a change to the retailing landscape with large format retailing – particularly foodstores – changing the function of the traditional high street towards a specialist destination with a greater social leisure function. The Council will continue to encourage town centre development that supports the high street

2.37 The district’s towns provide the best access to employment, services and shops. Glastonbury town centre satisfies the basic shopping needs of local people whereas the other centres offer a broader range and choice of goods. Street has a wider sub-regional offer due to the Clarks Village outlet centre. Nevertheless opportunities exist to improve shopping, particularly in Wells and Frome.

2.38 The close proximity of Glastonbury and Street means that together they provide enhanced access to services and together provide the second greatest concentration of jobs in the district. Shepton Mallet Town Centre remains the weakest of the district centres and new efforts to encourage regeneration of the town centre are proposed through a Neighbourhood Plan being advanced by the Town Council which intends to encourage key landowners to work more closely to reshape the offer of the town.

2.39 The other main growth sectors include Construction, Health and Other Services with the latter including a range of arts, entertainment and recreational activities. Hospitality (made up of hotels, restaurants) contributes to the wider tourism economy. Visitors to the district spend an estimated £161 million a year. 2010 data indicates that 3,570 jobs are directly related to tourism enterprises, however this understates the contribution made by pubs, restaurants and other visitor orientated businesses that also serve the local population. The district has a number of attractions of regional significance, including Glastonbury Tor and Abbey, Wookey Hole Caves and Wells Cathedral, and the high quality natural and built environments already act as a major draw to the area. One of the biggest challenges for tourism in the district is to increase the quality on offer and to translate a large number of day visits to overnight stays and longer breaks.

2.40 The annual Glastonbury Festival at Pilton, near Shepton Mallet remains the largest regular music festival in the country attracting over 100,000 people. It is estimated to be worth £73m to the local economy. Nearby, at the Bath and West Showground, agricultural shows, exhibitions and other events draw even larger numbers throughout the year offering potential to tap into. The Royal Bath and West Society have set out a clear regeneration plan to modernise the site and accommodate new business growth, offering improved conference space and exhibition buildings, with the aim to stimulate the site as a showcase of rural activities including food producers, outdoor activities and renewable energy alongside their core agricultural show role.

2.41 Access to most services can be achieved in each of the five Mendip towns although the increasing scale of Frome as a town means that there is greater need to provide more effective intra urban public services as well as further extending foot and cycle links with the River Frome Corridor being seen as an opportunity in this respect. Delivering a wider network of walking and cycling routes is a goal in each of the towns based on community consultation. Across the district there are examples of community groups, supported by Sustrans, who are working towards delivery of multi-user paths utilising, where possible, former railway corridors.

2.42 Across rural areas the availability of services in villages is varied. Larger communities like Evercreech, Beckington and Chilcompton have a good range of services allowing people to meet a wide range of daily needs. In others, facilities are limited to the basics, namely a shop, primary school, pub and bus service whilst in the scattered remaining villages and hamlets services are less viable and common. Mendip’s villages, like so many across the country, have experienced a decline in the number of facilities and services, such as village shops, pubs and Post Offices. However, it is fair to observe that in reaction to the centralised, homogenised offer of the main supermarkets there are an increasing number of farm shops and similar enterprises which are creating new markets around local and specialist produce.

2.43 Transport is critical for Mendip’s residents, employers and providers of services. Frome is the only Mendip town to have a railway station and this provides good linkages to Bristol, Bath and the west Wiltshire towns along with services to Yeovil, Weymouth and London Paddington. There are frequent bus services between the towns and Wells has good onward connections to a variety of larger centres including Bristol, Bath and Taunton. Connections from Shepton Mallet to larger centres are less straightforward requiring journeys via Wells. Evening services are limited.

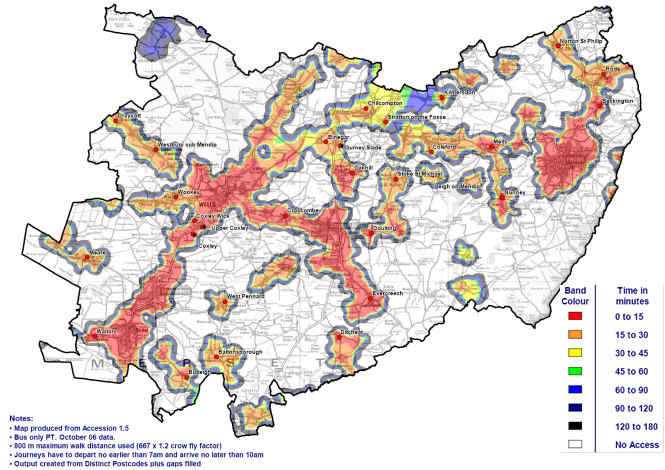

2.44 Rural services are varied. Where villages lie on or close to routes the bus can provide a reasonable alternative to the car. However, away from these villages services are less frequent and not suited to serving travel to work needs. The map below is a representation of accessibility by public transport to work in a nearby town before 10am on a weekday. Shaded areas illustrate zones where, with a short walk to a stop, a bus can get you to a town (inside or outside Mendip) whilst the white areas are those where standard public transport would not be feasible. Dial-a-ride services also cover the district but capacity is limited and oversubscribed. Service cuts since 2010 have maintained services to the villages where development is planned, however services and frequency to smaller communities is noted to have declined.

FIGURE 6: Accessibility by Public Transport to a Town before 10am on a weekday

2.45 Rates of car ownership are relatively high but, because of the multi-centric nature of the district, patterns of rural travel do not generate substantial congestion flow along specific road corridors. Mendip is not however, immune from congestion. Pinch points on the road network exist at Glastonbury using the A361, whilst at peak times travel within Frome can be delayed. Local views indicated that in Frome, travel outwards to Bath and west Wiltshire combined with a large amount of school traffic (on account of the distribution of schools) is the cause. Whilst observation bears this out, there is evidence that suggests that a high proportion of pupils in Frome walk to school.

2.46 In terms of priorities for highway investment, the eastern approach to Glastonbury via Chilkwell Street and the Walton Bypass, west of Street remain important schemes and, at Frome, a western relief road to divert heavy goods vehicles approaching from the A362 which pass through the town remains a long held aspiration.

2.47 Parking provision has remained a sensitive issue with government policy in the last decade aimed at reducing parking provision to dissuade car use and stimulate the use of public transport, walking and cycling. Under provision associated with new residential development has stretched on-street parking in some towns, notably Frome and Glastonbury, whilst in Wells parking to serve the town centre remains a pressure point which an allocation in the last Local Plan has not delivered. Many views from consultation also highlighted parking charges as a barrier that town centre shops had to endure which supermarkets and retail parks did not.

2.48 Broadband coverage is an important means for people to work from home and access services from more remote locations as well as being a key form of infrastructure to stimulate the local economy. Away from the towns, coverage is currently poor and business interests highlight that without this key infrastructure, the ability of people to establish small businesses will be stifled. In 2011, a bid for specific funding by councils in Somerset and Devon to secure accelerated delivery of “unlimited broadband” delivering speeds of up to 100MB/sec was successful and the first stages of that rollout will begin in 2013.

2.49 The district’s main centres have varied social, cultural and leisure facilities. Frome has a significant cultural offer with two theatres, a cinema, the Cheese and Grain - which offers a venue for live music - as well as a museum and a range of art establishments. Wells has a cinema and a range of local groups and societies, actively supported by sections of the community whilst at Street, Strode Theatre offers a performance venue associated with the college. Shepton Mallet is arguably less well provided for in terms of cultural venues with attempts to bring the Amulet Theatre back into use being dogged by financial constraints.

2.50 Social leisure, in terms of pubs, bars, restaurants and other venues to provide people of all ages with places to meet, eat and revel is varied across the district. Across rural areas the village hall and local pubs remain at the heart of rural communities although the availability of cheap supermarket alcohol continues to erode viability. Within the towns the traditional pub still has a place however the range of activities sought has broadened to bars, restaurants and clubs which are common place in centres like Bath, Yeovil and Taunton. The town centres study suggests that there is scope for operators to find niches in Mendip although opportunities will depend upon trading conditions and the right site. On the face of it Street (with its Quaker roots that limited commercial leisure development) and Frome (with its proportionately greater population) appear to have the greatest potential to attract this type of investment as both are relatively underprovided for.

2.51 Open space and provision for sport is reasonable across the towns. Deficiencies exist in particular types of spaces as detailed in the Council’s Play Strategy and Open Space Assessment although planned provision in line with future development can address these needs. The towns and villages have various sports clubs, including bowls, netball, cycling, golf, football, rugby and cricket, although in some cases, notably Street and Shepton Football Clubs and Wells Rugby Club, investment in facilities is needed to maintain support and encourage participation.

2.52 Physical sports infrastructure like sports halls, swimming pools and the like are under financial pressure. Local authority provision in Mendip, through managed contracts, remains the subject of review. Pressures exist and will arise for investment to refurbish or replace facilities and costs, particularly energy costs, for swimming facilities continue to rise. The conclusion of the review will make recommendations about how future provision should be best made across Mendip and the planning framework will facilitate that during the Local Plan Part II: Site Allocations process if required.

2.53 In terms of cultural heritage the district is blessed. Wells, with its ecclesiastical heart and fine townscapes, and Glastonbury, with the iconic Tor and Abbey steeped in history and legend, stand out but there is so much more. Frome, Shepton and Street also have important and impressive heritage with potential to further exploit in a sensitive manner. And, across rural Mendip, the caves at Wookey Hole, the Somerset Levels, the East Somerset Railway and the Mendip Hills exist within the varied landscapes that in themselves people like to visit, enjoy and walk.

Environment:

People:

Housing:

Economy:

Accessibility & Transport:

Culture and Leisure

|

< Previous | ^ Top | Next >